Market Exposure Model

Equities continued to advance in June following more evidence of cooling inflation and renewed expectations of policy rate cuts. The S&P 500 and the Dow climbed by 3.6% and 1.2%, respectively, while the technology-heavy Nasdaq outperformed by rallying 6.0% for the month. Markets seem optimistic about the outlook of easing policy, pricing in two interest rate cuts this year, while the median dots from the FOMC suggested only one cut. We believe that we are in a higher-for-longer interest rate environment and expect a shallow path for rate cuts, given prospects for moderate economic growth and a bumpy road towards slower inflation. Also, there is an extreme level of stock concentration, with the largest 20 stocks accounting for 75% of S&P 500 gains year to date. While we expect technology to continue fueling economic growth, we remain cautious and view this trend as unlikely to be sustained. Overall, we anticipate a bumpy process in the “last mile” on inflation, high for longer policy rate, and moderating growth. With this backdrop, we maintained an allocation to U.S. equities at 48%.

Stock Scoring Model

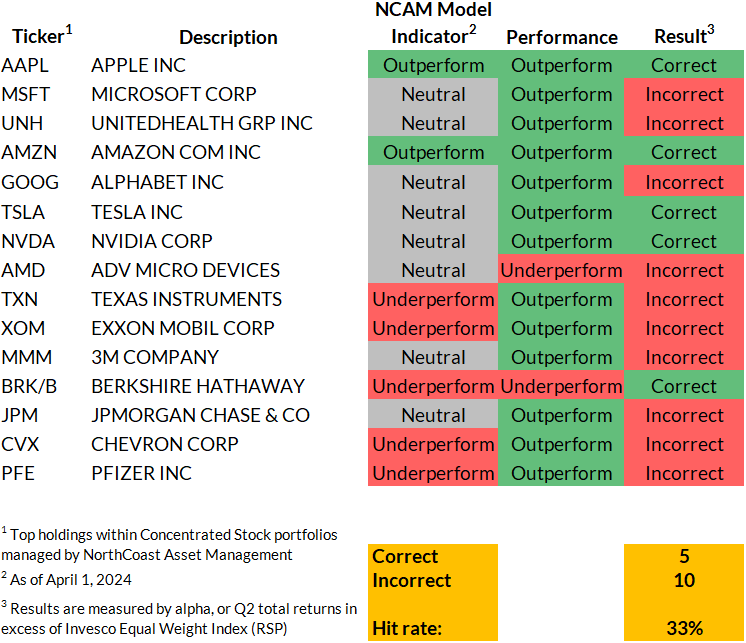

Of the top holdings within the Concentrated Stock portfolios, our stock scoring model had a hit rate (or “success rate”) below average last quarter. The model generally predicted neutral or underperformance against the Invesco Equal Weight Index (RSP). We anticipated that iPhone manufacturer Apple (AAPL) would outperform due in large part to management behavior. Shares rallied following CEO Tim Cook’s positive comments on plans to expand the usage of AI (artificial intelligence) in its devices and record $110 billion share repurchase announcement. Shares outperformed RSP by 25% during the quarter.

Outlook on UnitedHealth (UNH) was neutral. Medical costs and operating expenses have grown significantly higher. Earlier this year, the company fell victim to a cyberattack and the U.S. Department of Justice launched an antitrust investigation into the company. However, shares pared losses from the early part of Q2 when it was reported that earnings and revenues beat estimates. Shares outperformed the RSP by 6.0% in Q2.

Options Pricing Model

Portfolio Insights: NorthCoast’s Triple Play Strategy, A Multi-Faceted Approach to Options Strategies

While some investment advisors may implement a market-agnostic style when managing option overlay portfolios, the NorthCoast team employs the Triple Play strategy, which incorporates market outlook, stock score, and option pricing models to help select optimal options contracts.

Market Exposure Score

The first input is the market exposure score. At the start of Q2, our score was 57%, a conservative outlook. The score ranges between 0% and 100%. The higher the score, the more optimistic the model outlook. The lower the score, the more pessimistic the outlook.

One of the reasons for this score is that valuation metrics for equity remained negative. Price-to-earnings (P/E) ratios (historical and forward) inched higher. Sentiment was also negative. U.S. manufacturing activity contracted. The University of Michigan Consumer Confidence Index fell sharply as elevated gasoline prices and stubborn inflation weighed on consumer outlook. Technical indicators were positive, with encouraging momentum signals outweighing neutral reversal signals. Further, the S&P 500 was 12% above its 200-day moving average. The VIX (volatility index) was relatively flat with low realized volatility. Lastly, macroeconomic fundamentals were neutral. Nonfarm payrolls rose by 272,000 in May, stronger than consensus expectations. The initial jobless claims drifted upwards, with the four-week moving average edging up to 236,000 as of June 22.

Stock Score

Stock scores are based on valuation, comprehensive value versus peer group, sentiment, institutional attention, market efficiency, technical indicators, and management behavior. These components make up the composite score. A higher score indicates a greater confidence level of outperformance, whereas a lower score estimates greater likelihood of underperformance.

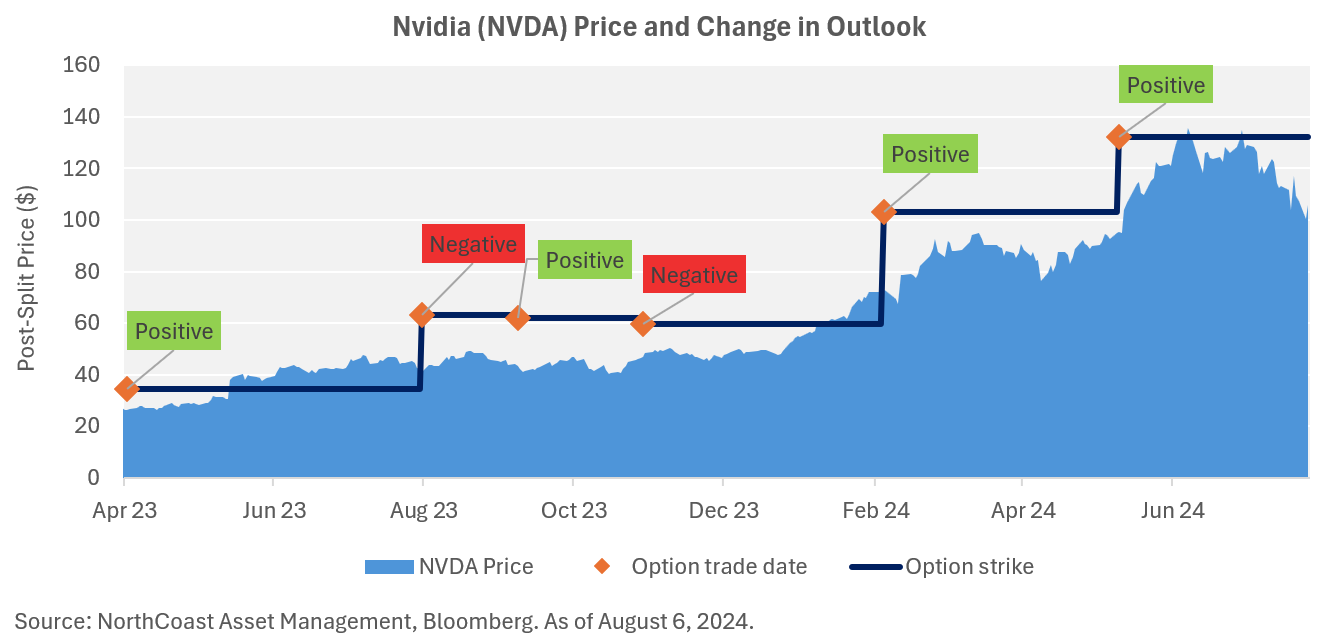

To illustrate, our score on NVIDIA (NVDA) earlier this year was 87%. The company is known primarily for designing and manufacturing graphics processing units (GPUs). NVDA made headlines last year following blowout earnings due to the AI revolution and demand for its products. Valuation, relative value versus peer group, and management behavior looked positive. Additionally, the company saw four consecutive quarterly earnings beats (when earnings were greater than expectations), strong top-line revenue growth with net profits, and positive guidance.

Options Pricing Model

In the first half of the year, we observed several spikes in the implied volatility of NVDA call options, and a higher figure typically leads to greater option yields. We used these opportunities to capture attractive option premiums and keep strike prices elevated while the outlook on NVDA was positive.

Putting Together the Pieces

The below graph shows NVDA’s price over the past year with changes in outlook and option trades. When projections for the market and NVDA were positive, we maintained a high level of strike prices or moved even higher. When the outlook was negative, we opted to lock in option gains, moderately lower strike prices to capture more yield, and roll options further out for additional cash flow.

Our experience has shown that incorporating a market view and stock score is a more effective way of managing covered call option strategies.